Small business margins are tight. With recent legislative changes including the massive One Big Beautiful Bill Act (OBBBA) provisions, and constantly evolving IRS regulations, relying on outdated tax advice means you are leaving serious money on the table.

But here is the core theme of tax strategy: You cannot claim what you cannot prove. Maximizing your write-offs requires pairing elite tax knowledge with a real-time expense tracking system. The IRS operates on the burden of proof, meaning you only get to keep your tax savings if you have the receipts to back them up.

In this guide, we’ll break down the top 25 tax deductions for 2026, the latest One Big Beautiful Bill Act (OBBBA) updates, and how to automate your compliance so you never lose an audit.

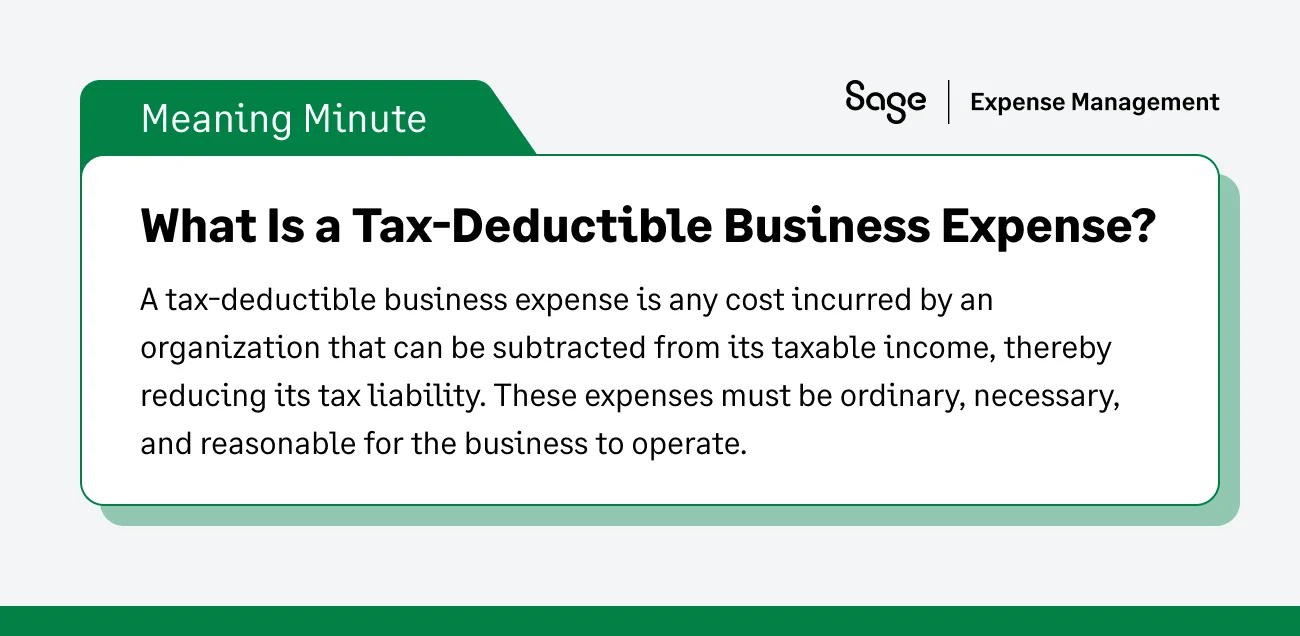

What is a Tax Deduction?

A tax deduction is a qualifying business expense that you subtract from your company's gross income. By reducing your gross income, you lower your overall taxable income, which ultimately reduces the amount of tax you owe.

Example: If your business earned $150,000 this year, but you have $30,000 in qualifying deductible expenses, you will only pay taxes on $120,000.

{{smb="/did-you-know-cards"}}

How Do Tax Deductions Help Businesses?

On the surface, tax deductions save you money so you can reinvest in your growth, hire top talent, and stay compliant. But for many founders, there is a hidden layer of savings.

The double tax secret: For sole proprietors and single-member LLCs, business expenses are deducted on Schedule C before your net profit is calculated. This means deductions don’t just lower your federal and state income tax; they also directly reduce your Self-Employment (SE) tax (which is a hefty 15.3% for Medicare and Social Security).

Every dollar you deduct works double-duty to save you cash!

(Note: This refers purely to operational SE tax savings, not international Double Taxation Avoidance Agreements.)

What Qualifies as a Tax Deductible Expense?

Under IRS rules, to be deductible, a business expense must be both "ordinary and necessary".

- Ordinary: An expense that is common and accepted in your specific industry.

- Necessary: An expense that is helpful and appropriate for your business. (It doesn't have to be strictly indispensable to qualify).

Examples include utilities, office supplies, and wages. Expenses that are partly personal and partly business-related, such as internet costs, may be partially deductible. Accurate record-keeping is essential for claiming these deductions.

Tax Deductions vs. Tax Credits: Which Saves You More?

While a tax deduction reduces your taxable income (meaning your actual cash savings depend on your specific tax bracket), a tax credit is a dollar-for-dollar reduction of your actual tax bill.

If you owe $15,000 to the IRS and get a $5,000 tax credit, your bill drops exactly to $10,000. A smart financial strategy utilizes both.

The 26 Essential Small Business Tax Deductions

Here is a list of the most common small business tax deductions you should take advantage of for your small business:

1. Home office expenses

If you work from home, you can deduct a percentage of your rent, mortgage interest, property taxes, and utilities.

- The Rule: The space must be used exclusively and regularly as your principal place of business according to IRS publication 587.

- The Exceptions: You do not need to meet the strict exclusive-use test if you use the space for the Storage of Inventory (a huge win for e-commerce founders) or if you operate a licensed Daycare Facility.

- The Calculation: You can use the Actual Expense method or the Simplified Method (a flat $5 per square foot up to 300 square feet, maxing out at $1,500).

2. Business property rent

If your business rents a physical location, office space, or equipment, the rental payments can be fully deducted as a business expense. This deduction applies to various rentals, including long-term leases and short-term equipment rentals essential for business operations.

What qualifies

- Rent for office spaces, retail shops, warehouses, or equipment used exclusively for business.

- Storage units or other facilities used for inventory or supplies.

What doesn’t qualify

- Rent paid for a personal residence, even if you have a home office. These expenses must instead be included under home office deductions if eligible.

- Lease-to-own payments where you eventually gain ownership of the property are not deductible as rent; they must be treated as capital expenses.

Unreasonable rent

The IRS disallows deductions for “unreasonable” rent, typically in cases where the landlord is a related party and charges above-market rates.

Advance rent warning

You cannot deduct advance rent payments in the year you pay them. You cannot prepay 2026's rent in December 2025 just to get a year-end write-off.

3. Utilities

Electricity, water, gas, and internet services for your commercial space are fully deductible. If you work from home, you split this based on your business-use percentage.

For example:

- If 40% of your internet use is for business, you can deduct 40% of the cost.

- Detailed records, such as bills and usage logs, can help justify this deduction during audits.

4. Office supplies

Office supplies are day-to-day items necessary for running a business. They are fully deductible if purchased and used within the same tax year.

Also, in the cases of supplies such as laptops, instead of depreciating moderately priced assets over several years, the De Minimis Safe Harbor rule allows you to immediately expense items that cost $2,500 or less per invoice.

What qualifies as office supplies?

- Basic supplies: Paper, pens, notebooks, printer ink, staplers, and cleaning products.

- Electronics and Equipment: Computers, printers, and monitors. High-cost items may need to be depreciated or deducted under Section 179 instead.

Tips for tracking office supply expenses:

- Keep receipts and invoices for every purchase.

- Categorize expenses in your accounting system for easier tax reporting.

- Use tools like Sage Expense Management to streamline tracking and ensure no expense is overlooked.

5. Office furniture

Office furniture is considered a type of office supply and can be deducted similarly to other office expenses like printer paper or cleaning products. Therefore, purchasing furniture for your small business will fall under deductible business expenses on your tax return.

For example- desks, chairs, whiteboards, and filing cabinets purchased to furnish your workspace are deductible.

6. Software subscriptions

If you have purchased or downloaded software for your business, remember that these are deductible business expenses from your tax return. This type of expense can be claimed under the “Other Common Business Expenses>Other Miscellaneous Expenses” category on your Schedule C tax form.

7. Advertising and Marketing

As long as you have evidence that advertising and marketing expenses are related to your small business, you can claim a tax deduction for the money spent. This includes money spent on billboards, business cards, direct mails, or hiring a freelancer to design a business logo.

8. Energy efficient commercial buildings deduction

If you own a commercial building, going green can save you serious green. The Section 179D deduction rewards building owners who make qualifying energy-efficient upgrades.

- The Rule: You must increase the overall energy efficiency of your building by at least 25%. The upgrades must apply to specific internal systems: interior lighting, HVAC (heating, cooling, ventilation), or the building's physical envelope (like windows, doors, and insulation).

Let's say you own a retail warehouse. You decide to completely overhaul the outdated HVAC system and install smart LED lighting. An independent engineer certifies that your building's total energy use just dropped by 30%. You can now claim a massive tax deduction calculated by the total square footage of your building.

9. The SALT cap update

If you live in a high-tax state like California, New Jersey, or New York, you likely remember the sting of the old $10,000 cap on State and Local Tax (SALT) deductions. Thankfully, the new One Big Beautiful Bill Act (OBBBA) brings massive relief.

- The new rule: The SALT deduction cap has officially been increased to $40,000 for eligible taxpayers (or $20,000 if you are married filing separately).

- What this means for you: When you itemize your personal tax return, you can now deduct up to $40,000 of the property taxes and state income taxes you paid during the year. Because business profits from LLCs and sole proprietorships flow through to your personal tax return, this higher cap directly protects a huge chunk of your business income from federal taxation

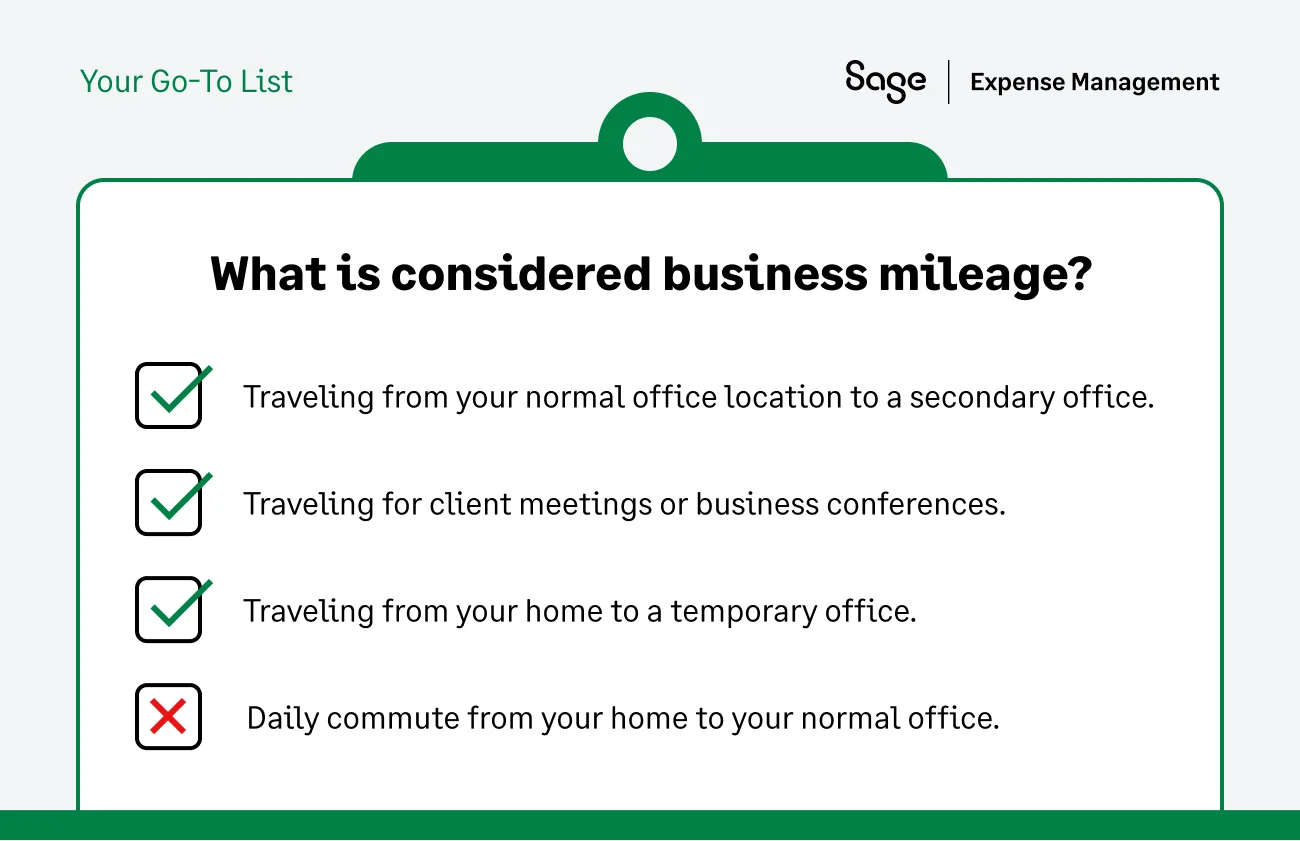

10. Auto expenses

If you drive for business, you can deduct vehicle costs using either the Standard Mileage Rate (72.5 cents/mile for 2026) or Actual Expenses (gas, oil, repairs, lease payments).

Pro Tip: You must choose the standard mileage rate in the very first year the car is available for business use. If you use the actual expense method in year one, you lose the right to ever use standard mileage for that specific vehicle.

What counts as business mileage?

Record-keeping requirements:

- Maintain a mileage log with dates, destinations, business purposes, and mileage for each trip.

- Keep receipts for fuel, repairs, and other auto-related expenses if using the actual expense method.

Also read-

11. Travel expenses

Business travel (airfare, hotels, rental cars) is deductible, but with caveats.

Business-related travel expenses are deductible, but they must meet certain criteria to qualify.

Examples of deductible travel expenses

- Transportation: Airfare, train tickets, rental cars, and mileage for personal vehicles used for business.

- Lodging: Hotel stays while traveling for business.

- Meals: Deductible at 50% for business trips.

- Incidental Expenses: Tips, dry cleaning, baggage fees, and internet charges.

Requirements for deduction:

- The travel must be primarily for business purposes.

- The trip must take you away from your tax home (the city or area where your business is based).

- Personal activities during the trip, such as sightseeing, are not deductible.

The sleep or rest rule: You cannot deduct travel if you just drive 3 hours away for a meeting and come back the same day. Your duties must require you to be away from your tax home substantially longer than an ordinary day's work, requiring you to stop for sleep or rest.

{{stop-guessing="/cta-banners"}}

12. Business meals

Business meals are strictly subject to a 50% limit. The pandemic-era 100% rule is dead. The IRS allows businesses to deduct the cost of meals incurred while conducting business, but there are rules and limitations.

Deduction rules:

- Standard deduction: 50% of the meal cost is deductible. However, some meals, such as those provided at office parties or during recreational events, are 100% deductible.

- Business purpose: The meal must be directly related to business discussions or activities.

What to document:

- Date and location of the meal.

- Names and roles of attendees.

- Purpose of the meal and its connection to business activities.

Examples of deductible meals:

- Lunch meetings with clients to discuss projects.

- Meals provided during a training seminar for employees.

- Office holiday parties or team-building dinners (100%)

13. Client gifts

Yes, you can deduct the cost of gifts you give to clients, customers, and vendors. But the IRS is remarkably stingy here.

- The Rule: You are legally capped at deducting a maximum of $25 per person, per year. If you send a top client a $100 gourmet holiday basket, you can only write off $25 of it. The remaining $75 is completely non-deductible.

- The incidental exception: Incidental costs do not count toward your $25 limit. This includes expenses for custom engraving, gift wrapping, insuring, and shipping. So, if you buy a $24 item, pay $5 to wrap it, and $10 to ship it, the entire $39 is deductible because the core gift was under $25.

- The company swag exception: What if you hand out branded merchandise at a trade show? Items that cost $4 or less like pens, tote bags, or coffee mugs do not count toward the $25 limit, provided your company name is permanently imprinted on them and you distribute them widely.

- Gift vs. Entertainment warning: Be very careful giving tickets to a sporting event or concert. Even if you just hand a client the tickets as a "gift," the IRS generally classifies this as an entertainment expense. That means it drops to 0% deductible.

14. The Entertainment myth

Entertaining clients or employees can boost morale and foster relationships, and the IRS allows certain business entertainment expenses to be deducted. Many founders mistakenly believe taking a client to a football game or concert is a write-off.

Rules around deducting business entertainment expenses

- 50% Deductible

Most client-related meals or entertainment events fall under this category. Examples include taking a client to a sports game or hosting a business lunch.

If you buy food or drinks at an entertainment event, the food is 50% deductible, but only if it is billed separately from the event tickets.

- 100% Deductible

- Meals provided during office events, such as holiday parties or team-building activities, are fully deductible.

- Meals included in business-related recreational activities primarily benefiting employees, such as a company picnic.

What doesn’t qualify

- Extravagant or personal entertainment, such as vacations or non-business-related outings.

- Entertainment where no business discussion takes place or is incidental to the activity.

Pro Tip: Document every detail, including the purpose, attendees, and receipts. IRS scrutiny on entertainment expenses is high, so keep thorough records.

15. The EV sunset

If you were planning to green your commercial fleet and cash in on the popular Clean Vehicle Credit, you need to hit the brakes.

- Under the new One Big Beautiful Bill Act (OBBBA), the tax landscape for electric vehicles drastically changed. Most federal tax credits for electric and fuel cell vehicles were completely eliminated for any vehicle acquired after September 30, 2025.

- This means buying a standard electric delivery van today will no longer give you that dollar-for-dollar tax credit. If your business needs to upgrade its fleet this year, you should pivot your tax strategy.

Instead of chasing dead EV credits, look into maximizing the Section 179 deduction by purchasing heavy vehicles (like trucks or SUVs over 6,000 pounds) to secure massive first-year write-offs.

16. The Fuel Tax credit

Every time you buy gas or diesel for your business, you are paying federal highway excise taxes that are secretly built right into the price at the pump. But what if you aren't actually driving on the highway?

The Rule: If your business buys fuel for off-highway business use, you shouldn't have to pay highway taxes. The IRS allows you to claim a refundable tax credit to get those federal excise taxes back.

Let’s say you run a construction or landscaping company. You buy hundreds of gallons of diesel fuel to run stationary generators, backhoes, or riding lawnmowers. Because that fuel never touches a public highway, you can file Form 4136 with your tax return to claim a direct, dollar-for-dollar credit for the excise taxes you paid.

17. Employee Wages

Paying employees is a major business expense, but wages, salaries, and certain employee benefits are deductible. The OBBBA introduced new Tax-Free Overtime and Tax-Free Tips provisions. While these are tax-free for the employee, it fundamentally changes how businesses must calculate their deductible wage base and payroll tax matching.

What qualifies as deductible wages?

- Salaries paid to employees who are not owners or partners in the business.

- Bonuses, commissions, and benefits paid under a pre-agreed structure.

- Vacation and sick pay, provided it aligns with your employment policies.

Tests for deductibility

- Reasonableness test: Wages must be reasonable for the services performed. Excessive pay may be disallowed.

- For services rendered: Payments must directly relate to work performed by the employee.

Filing requirements

- Report wages using Form W-2 for each employee.

- File copies of the W-2 with the IRS and Social Security Administration (SSA).

18. Contracted Labor

If you use independent contractors or freelancers as part of your labor force, the cost of hiring contracted labor is a tax-deductible business expense.

You must issue a Form 1099-NEC (not a 1099-MISC) for contractor payments of $600 or more according to IRS publication 535. Additionally, the 1099-K reporting threshold for third-party payment networks has officially been reverted to $20,000 (reversing the controversial $600 threshold attempt).

19. Employee Benefits Programs

Providing employee benefits not only boosts morale but also offers significant tax advantages for businesses. Contributions towards benefits like healthcare, retirement plans, and education assistance are deductible.

1. Health insurance contributions

- Premiums paid for employee health coverage under a qualifying arrangement are deductible.

- Small businesses offering health coverage through the SHOP Marketplace may qualify for the Small Business Health Care Tax Credit.

2. Retirement contributions

Contributions to employee 401(k) plans, SIMPLE IRAs, or SEPs are deductible.

3. Other benefits

- Dependent care assistance programs.

- Pre-tax deductions under Section 125 for health savings accounts (HSAs) and flexible spending accounts (FSAs).

Additional benefits

- Employers providing paid leave may qualify for a credit of 12.5% to 25% of the wages paid during the leave period.

- Student Loans: Employers can provide up to $5,250 tax-free per year to pay off an employee's qualified student loans according to IRS publication 970.

- Trump Accounts: The OBBBA introduced a brand-new fringe benefit of $5,000 tax-advantaged accounts for children that employers and authorized individuals can contribute to.

20. Self-Employed health insurance & QSEHRAs

If you are self-employed, you can generally deduct health insurance premiums for yourself and your family. If you have a small team without group health insurance, look into QSEHRAs (Qualified Small Employer Health Reimbursement Arrangements). You can reimburse employees tax-free for their own premiums, up to strict limits (e.g., $12,800 for families).

21. Business start-up & Organizational costs

The IRS allows you to deduct up to $5,000 in business start-up costs (marketing, travel) and $5,000 in organizational costs (legal fees) in your first year of business. This double-deduction phases out dollar-for-dollar if your total start-up costs exceed $50,000.

22. Bad Debts

Bad debts arise when you are unable to collect money owed to your business, resulting in financial loss. These debts typically occur in situations where you have provided goods, services, or loans, but the payment is either partially or entirely uncollectible.

Deducting bad debts can help you offset the loss on your tax return, provided you meet the necessary criteria set by the IRS.

Examples of Bad Debts

Business bad debts may result from the following scenarios:

1. Loans to clients, suppliers, or employees

- If your business extends a loan to a client, supplier, or employee for a legitimate business purpose and the borrower fails to repay, the unpaid amount may qualify as a deductible bad debt.

- For example, a supplier who receives an advance to complete an order but fails to deliver the goods or refund the money would create a bad debt situation.

2. Uncollected payments from customers

- Businesses using the accrual method of accounting report income when it is earned, not when it is received. If a customer fails to pay for goods or services, the uncollected amount may be deducted as a bad debt.

- For instance, an unpaid invoice for a large order delivered to a customer can be written off if the client defaults on payment.

3. Guarantees paid on behalf of another party

- If you guarantee a loan for a client or vendor and end up paying the loan on their behalf because they defaulted, this amount could also qualify as a bad debt.

- For example, a business owner guarantees a loan for one of their key distributors to maintain operations, but the distributor fails to repay the loan. The amount the owner repays on behalf of the distributor may be deducted as a bad debt.

The cash-method trap

If a customer doesn't pay their invoice, you might think you can write it off as a bad debt. However, if your business uses cash-basis accounting (where you only record income when cash is received), you cannot deduct unpaid invoices. Because the money was never recorded as income, you can't deduct its loss.

Key requirements for deducting Bad Debts

To qualify for a bad debt reduction, you must meet the following criteria:

1. The debt must be related to your trade or business

The debt must have been created or acquired as part of your business activities. For example, personal loans to friends or family members do not qualify, even if the loan was intended to help them start a business.

2. You must prove that the debt is worthless

- The IRS requires businesses to make a genuine effort to collect the debt before it can be considered bad. This includes sending payment reminders, attempting to renegotiate terms, and documenting all attempts to recover the debt.

- If a customer files for bankruptcy or repeatedly ignores collection notices, these can serve as evidence of worthlessness.

3. Documentation is essential

Keep thorough records of all relevant documents, including loan agreements, invoices, correspondence with the debtor, and evidence of collection attempts. This is crucial in case the IRS audits your deduction claim.

{{2022="/did-you-know-cards"}}

23. Child and Dependent Care

You can claim a tax deduction on your expenses for caring for your children or adult dependents. If you have children who are 12 years old or younger, deduct the expenses associated with their care.

Adult dependents, including spouses and certain other related adults who are unable to care for themselves due to physical or mental disability, also qualify for deductions.

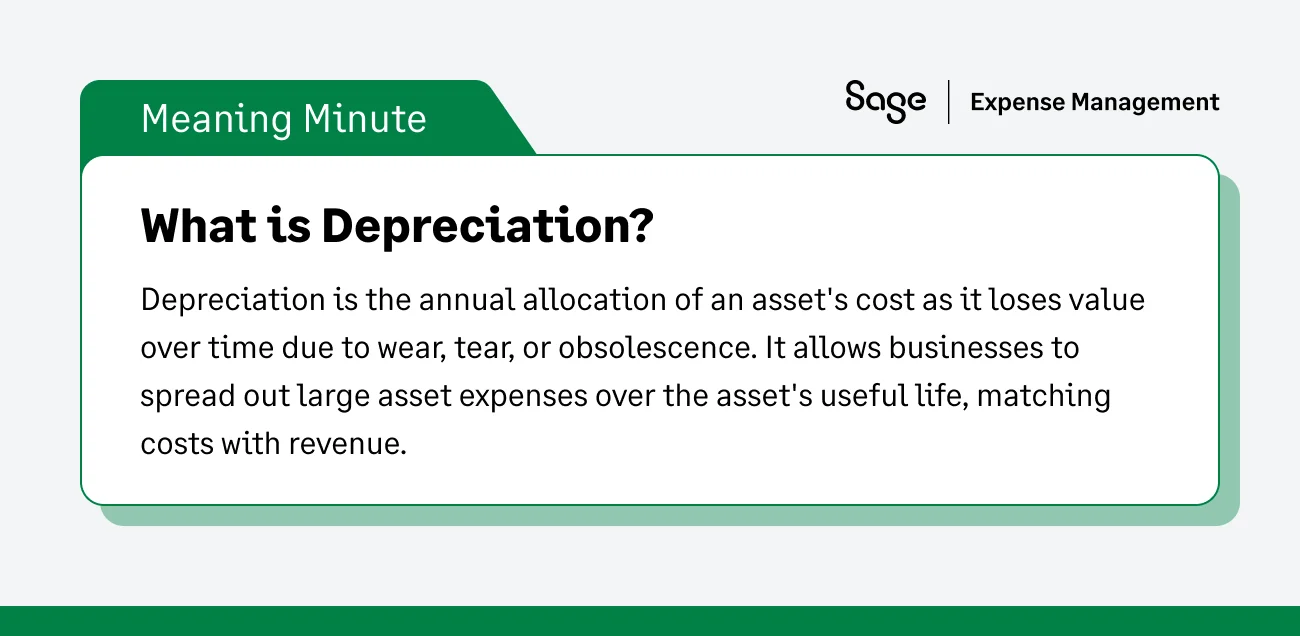

24. Depreciation

When you buy massive assets, you deduct their cost over time. Depreciation is a tax deduction that enables businesses to recover the cost of tangible assets used in their operations.

Instead of deducting the full expenses in the year the asset is purchased, depreciation spreads the deduction over the asset’s useful life. This approach aligns with the gradual wear and tear or obsolescence that assets experience over time.

What can be depreciated?

Depreciation applies to tangible assets that:

- Are owned by the business: You must legally own the asset, even if it’s being paid for over time (e.g., through a loan or installment purchase).

- Are used for business purposes: The asset must be employed in your trade or business to produce income. Personal-use assets, such as a car used solely for commuting, are not eligible.

To bypass strict passenger car depreciation limits, many businesses purchase vehicles rated over 6,000 pounds. Under Section 179, you can expense up to $31,300 of a Heavy SUV in 2025.

- Have a determinable useful life: Assets must have a predictable lifespan exceeding one year. For example, machinery may have a useful life of 10 years, while computers might last 3-5 years.

- Deteriorate over time: Assets that don’t physically deteriorate, like land, cannot be depreciated. While it had been phasing down, the OBBBA reinstated 100% Bonus Depreciation for 2026, allowing businesses to write off the entire cost of qualifying equipment in year one again.

Examples of depreciable assets include:

- Buildings and improvements (excluding land).

- Machinery, tools, and manufacturing equipment.

- Office furniture, fixtures, and technology.

- Vehicles used exclusively for business.

- Intangible property like patents and copyrights (which are amortized instead of depreciated).

How to claim depreciation

- Identify assets eligible for depreciation and their costs, including installation or shipping fees.

- Choose the appropriate depreciation method (e.g., straight-line, Section 179).

- Complete and attach Form 4562 (Depreciation and Amortization) to your business tax return.

- Keep records of asset purchases, usage, and calculations for at least three years after filing.

25. Amortization & R&D

Amortization is a method of deducting the cost of certain intangible assets over a specified period, typically reflecting the asset’s useful life. It’s similar to depreciation but applies to non-physical assets such as patents, copyrights, trademarks, and startup costs.

Key points about Amortization

1. Intangible assets

These include legal rights or intellectual property that contribute to business operations. Certain intangible assets (like patents, trademarks, or goodwill) must be amortized over exactly 15 years (180 months) according to IRS publication 535

Examples: Trademarks, patents, goodwill, organizational costs, and software.

2. Straight-line deduction

Amortization spreads the cost evenly over the asset’s useful life. For instance, if you spend $15,000 to acquire a patent with a 15-year life, you can deduct $1,000 annually.

3. Startup costs

Costs incurred before starting operations (e.g., market research, legal fees, and training) can also be amortized over 15 years, provided they exceed $5,000.

Steps to claim Amortization

- Identify the qualifying intangible asset and determine its cost and useful life.

- Complete Part VI of Form 4562 to report amortization expenses for the current year.

- To substantiate the deduction, maintain documentation, such as purchase agreements or legal filings.

Research & Development (R&D) costs can now be expensed immediately in the year incurred, completely reversing the prior TCJA requirement that forced businesses to amortize them over 5 years.

26. Business Interest Expense

Normally, the IRS limits how much business interest expense a company can deduct. However, under OBBBA, if your business's average annual gross receipts for the previous three years are $31 million or less, you are completely exempt from the Section 163(j) limits. You can deduct 100% of your business interest.

9 Tax Credits for Small Business

Tax credits are a way to reduce the tax bill of your small business by a certain dollar amount or percentage of a specific cost, making them an effective way to alleviate tax liability. Let us take a look at various tax credits that you can benefit from:

1. Research and Development (R&D) Tax Credits

The R&D tax credit is designed to incentivize businesses to invest in innovation, including developing or improving products, processes, or software. This credit helps offset the costs associated with research and experimentation.

Qualifying activities:

- Developing new products, formulations, or software.

- Improving existing products, increasing performance, reliability, or efficiency.

- Conducting prototype testing or experimentation.

Ineligible activities:

- Research conducted after commercial production has started.

- Customizing existing products for individual customers.

- Activities performed outside the U.S.

How to claim:

Businesses use Form 6765 (Credit for Increasing Research Activities) to claim this credit. Eligible small businesses can also use the R&D credit to offset their Alternative Minimum Tax (AMT).

Normally, tax credits offset income tax. But the IRS allows "Qualified Small Businesses" (under 5 years old with less than $5 million in gross receipts) to apply up to $500,000 of their R&D credit directly against their payroll taxes.

2. Small Business Health Care Tax Credit

This credit is aimed at small employers offering their employees health insurance through the SHOP Marketplace. It can help alleviate the cost of providing coverage.

Eligibility criteria:

- The employer must have fewer than 25 full-time equivalent employees (FTEs).

- The average annual wages per employee must be less than $62,000 (for 2024, adjusted annually).

- The employer must pay at least 50% of the employee's health insurance premiums.

Credit amount:

- Up to 50% of premiums paid for small businesses.

- Up to 35% for tax-exempt employers.

How to claim:

Calculate the credit using Form 8941 and file it with your annual tax return. Excess credit amounts can often be carried forward to future years.

3. Work Opportunity Tax Credit (WOTC)

The WOTC rewards employers who hire individuals from targeted groups that consistently face barriers to employment, such as qualified military veterans or ex-felons.

Credit details:

- Generally equal to 40% of the first $6,000 in wages paid to the employee in their first year.

- The maximum credit jumps to a massive $9,600 per hire for certain qualified disabled veterans.

Eligibility criteria:

Employers hiring individuals from targeted groups (such as veterans, ex-felons, or SNAP recipients).

How to claim:

File Form 8850 (Pre-Screening Notice and Certification Request) with your state workforce agency within 28 days of the employee's start date, and claim the credit on your tax return.

4. Energy Efficiency Tax Credit

This credit rewards businesses for making energy-efficient upgrades to their facilities. It supports sustainability efforts while lowering tax liability.

Qualifying activities:

- Building Improvements: Earn up to $1.80 per square foot for improvements such as energy-efficient windows, lighting, or HVAC systems.

- Solar Investments: Claim a 26% credit for installing solar panels or other renewable energy solutions.

- Other Renewable Energy Projects: Wind turbines and geothermal heat pumps may also qualify.

How to claim:

Use the appropriate tax forms based on the type of improvement, such as Form 3468 for renewable energy credits.

{{energy-efficient="/did-you-know-cards"}}

5. Employer-Provided Childcare Credit

This credit incentivizes businesses to support their employees by providing or subsidizing childcare services.

Credit details:

- Equal to 25% of qualified childcare facility expenses (e.g., constructing, maintaining, or operating a childcare facility).

- Includes an additional 10% for referral services that connect employees with childcare providers.

- The credit is capped at $150,000 annually.

Eligibility criteria:

- Expenses must be directly related to providing childcare services for employees.

- Costs for facility improvements, training childcare workers, or paying higher wages to qualified childcare staff are eligible.

How to claim:

File the credit using Form 8882 (Credit for Employer-Provided Childcare Facilities and Services).

6. FICA Tip Credit

This credit is available to businesses in the food and beverage industry where tipping is customary. It allows employers to recover the 7.65% FICA taxes they pay on tips that exceed the federal minimum wage.

Eligibility Criteria:

- The business must employ tipped workers in the food or beverage industry.

- Tips must be reported by employees and used to calculate FICA taxes.

How to Calculate:

The credit equals the employer’s share of FICA taxes paid on tips beyond the federal minimum wage of $5.15/hour (the 2007 rate used for this calculation).

How to Claim:

File Form 8846 to calculate and claim the credit. Unused credits can be carried back one year or carried forward up to 20 years.

7. Small Employer Pension Plan Startup Costs and Auto-Enrollment

Small businesses that establish retirement savings plans can claim a tax credit for the costs of setting up and administering these plans.

Credit details:

- Up to $5,000 annually for three years for the costs of starting a SEP, SIMPLE IRA, or other qualified retirement plans.

- An additional $500 credit is available for automatic employee enrollment plans.

Eligibility criteria:

- Employers must have 100 or fewer employees, each earning at least $5,000 annually.

- The business must not have offered a similar plan in the past three years.

Qualifying costs:

- Setting up and administering the plan.

- Employee education about the benefits of the plan.

How to claim:

File Form 8881 (Credit for Small Employer Pension Plan Startup Costs) to claim the credit.

8. Opportunity Zones

If your business realizes a massive capital gain (like selling a piece of real estate), you can defer those taxes. By reinvesting the gain into a Qualified Opportunity Fund (QOF) that supports economically distressed areas, you can delay your tax bill.

Credit details:

- Defer paying taxes on capital gains by reinvesting them into a QOF.

- If you hold the QOF investment for at least 10 years, you may pay zero capital gains tax on the new appreciation.

Eligibility criteria:

Taxpayers who realize capital gains and reinvest them into an eligible QOF within 180 days of the sale.

Qualifying costs:

Recognized capital gains reinvested directly into a Qualified Opportunity Fund.

How to claim:

File Form 8997 (Initial and Annual Statement of Qualified Opportunity Fund (QOF) Investments) along with your federal tax return.

9. Rehabilitation Credit

Instead of knocking down an old building for your new headquarters, consider restoring it. The Rehabilitation Credit is a tax incentive designed to preserve historic buildings.

Credit details:

A tax credit equal to 20% of your qualified rehabilitation expenditures.

Eligibility criteria:

- The building must be a certified historic structure.

- The rehabilitation project must be officially certified by the National Park Service.

How to claim:

File Form 3468 (Investment Credit) to claim the rehabilitation credit on your federal tax return.

Compliance & Record Keeping: Protecting Your Write-Offs

It is not enough to simply know about these 26 tax deductions. To actually keep your tax savings, you have to prove them.

How to Avoid an IRS Audit: Documentation Best Practices

To claim any of the deductions listed above, you must have the records to back them up. An estimated approximation will instantly fail an IRS audit.

If you get audited, a line item on your credit card statement that just says "Amazon $400" is not enough. The IRS expects you to keep documentary evidence. This means you need itemized receipts, canceled checks, and mileage logs that clearly establish four key facts for every single expense:

- The exact amount

- The date of the purchase

- The place of the transaction

- The specific business purpose

How long should you keep them? You must generally keep your tax records and receipts for at least three years from the date you file your original return. Thankfully, the IRS accepts digital copies. This is exactly why using an automated expense tracking app to snap photos of your receipts is your best defense against an audit.

The $31 Million Rule: Is Your Business Exempt from Interest Limits?

Normally, the IRS strictly limits how much business interest expense a company can deduct. Large businesses are typically capped at deducting only 30% of their adjusted taxable income.

However, the tax code offers a massive exemption for small businesses. If your business's average annual gross receipts for the previous three years are $31 million or less, you are completely exempt from this harsh limit. This secures your right to deduct 100% of your business interest on loans and credit lines.

But here is the catch: you must have immaculate financial records to prove to the IRS that your gross receipts fall under that $31 million threshold. Keeping pristine, automated books directly protects your right to claim this massive deduction.

How Sage Expense Management Can Help with Tax Deductions

Managing small business taxes can be overwhelming, especially when it comes to identifying deductible expenses, tracking receipts, and ensuring compliance with IRS regulations.

Sage Expense Management simplifies this process, making it easier for small businesses to stay organized and maximize tax savings. Here's how its innovative features can help:

No Credit Card Switch Needed

Switching corporate banks is a massive headache for any small business. Thankfully, Sage Expense Management is completely card-agnostic. It integrates directly with your existing major business cards using real-time feeds (RTF).

- Instantly match transaction data with submitted receipts.

- Automate credit card reconciliation in under two minutes without requiring a switch to new cards.

- Provide accountants with visibility into unauthorized or policy-violating transactions in real-time.

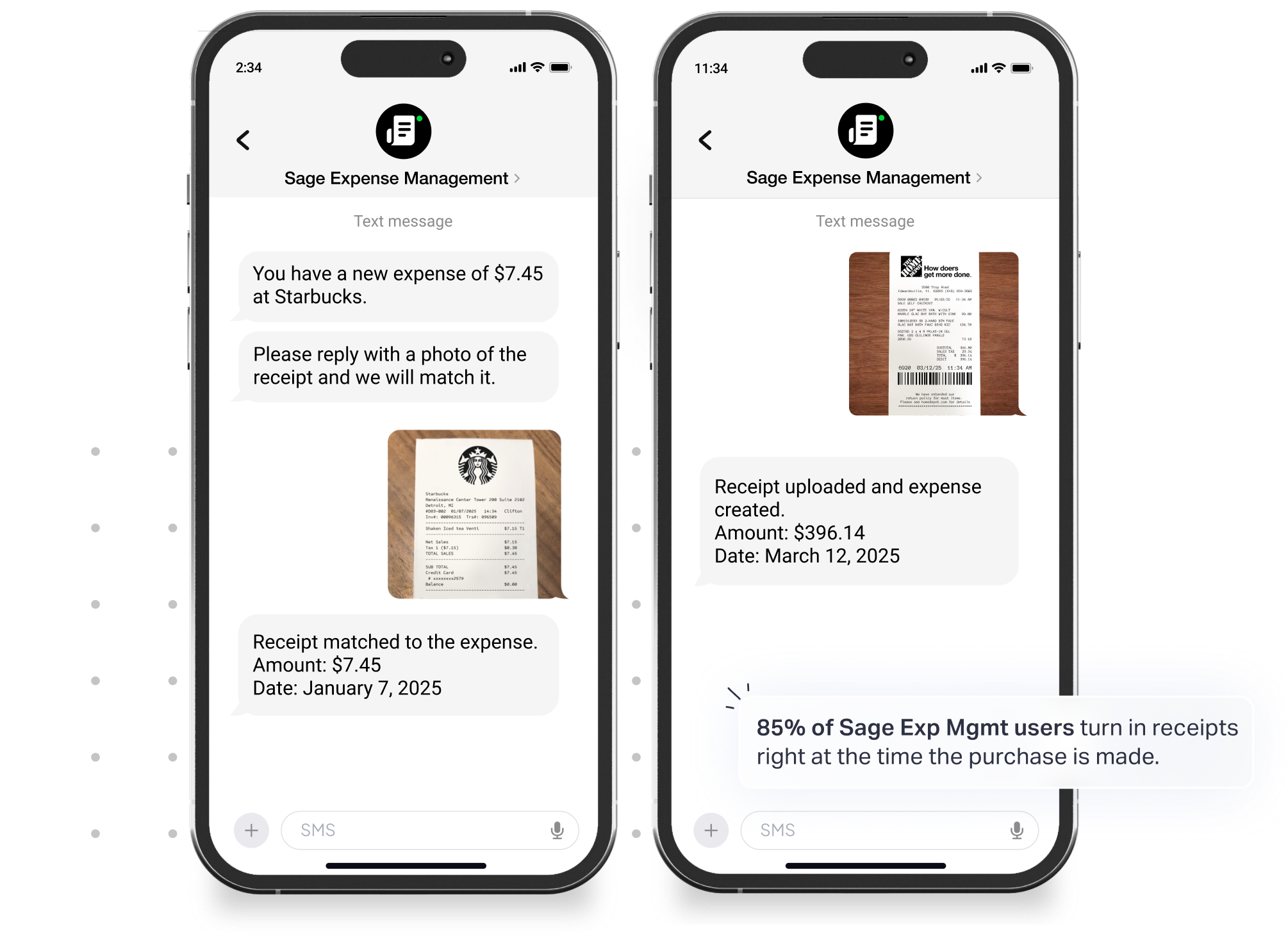

Stop Chasing Receipts

The IRS strictly requires documentary evidence to prove your business deductions. If you lose the receipt, you lose the deduction. Sage Expense Management solves this by sending an instant SMS text nudge to your employee the exact moment their card is swiped.

- Employees receive instant notifications for credit card transactions and can submit receipts via SMS or email.

- We supports receipt uploads from Gmail, Outlook, Slack, and Dropbox, making it effortless to track expenses in real-time.

- On average, businesses using Sage Expense Management reduced the time spent on receipt collection by 48%, minimizing back-and-forth communication between employees and accountants.

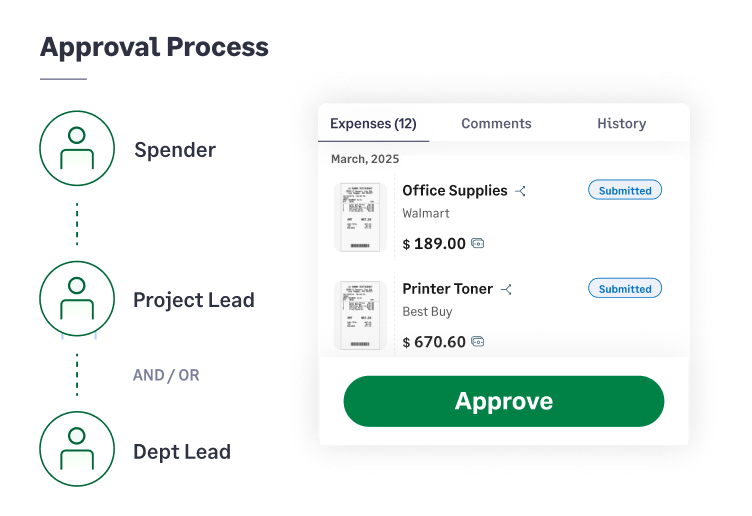

Automated Compliance & Multi-Level Approvals

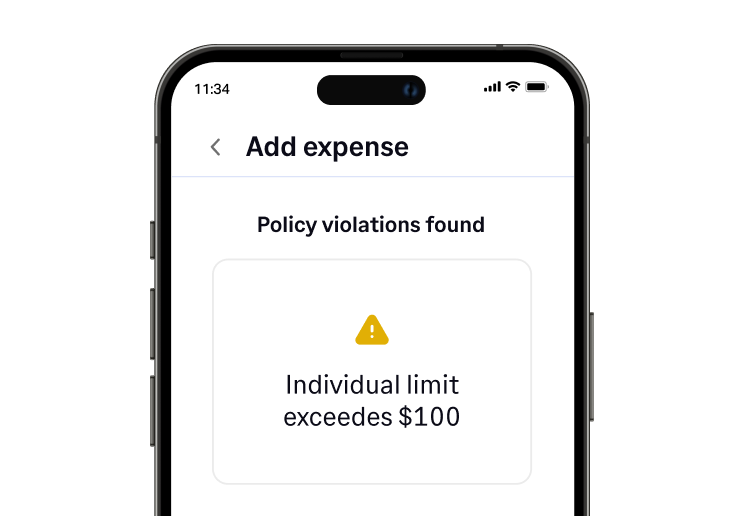

Want to prevent employees from accidentally expensing non-deductible items, like those 0% deductible expenses? Sage Expense Management automatically checks for policy violations, fraud, and duplicate entries before an expense is even submitted.

Furthermore, multi-level approval workflows ensure that managers can review project or departmental spend with a single click.

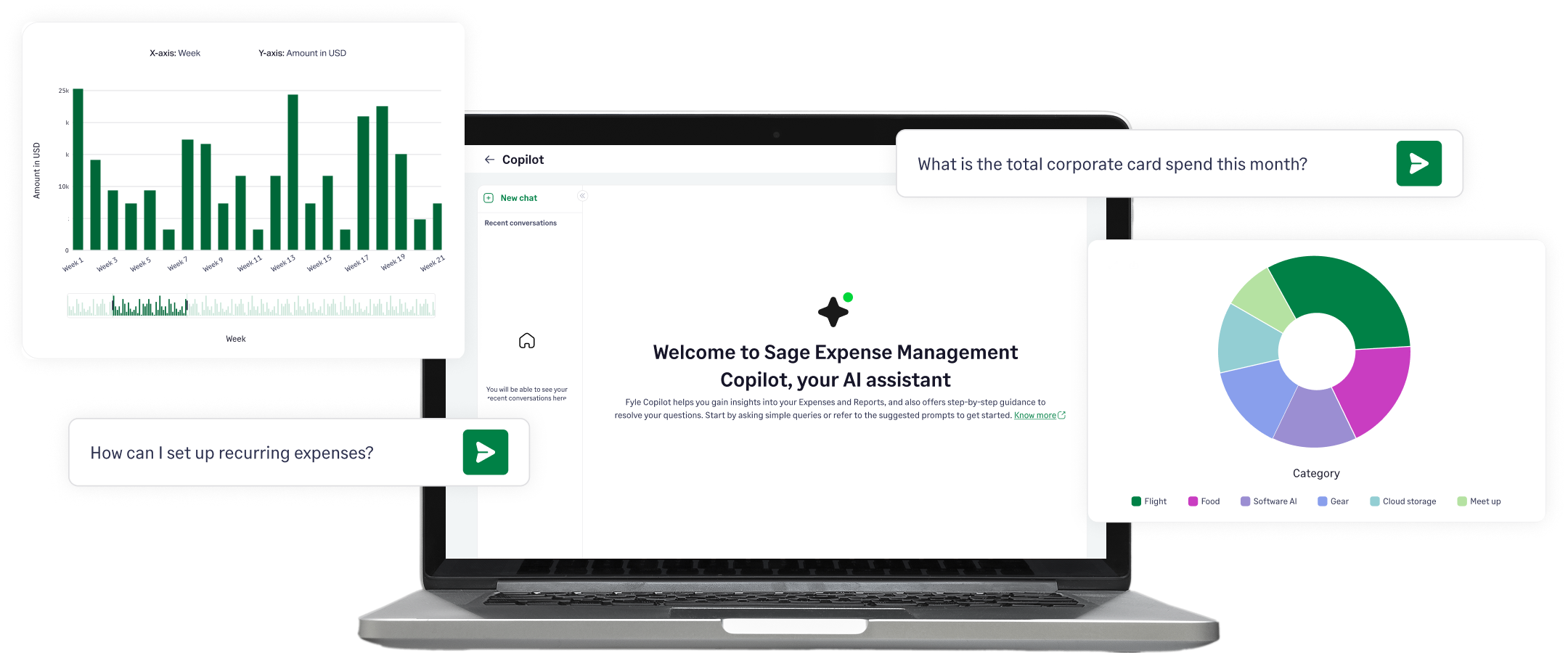

Simplified Tracking & Insights

Tax time is all about categorization. From utilities and office supplies to travel expenses, the platform streamlines expense tracking across all deductible categories:

- Use the spend overview dashboard to analyze expenses by category, department, project, or merchant.

- Allocate costs to specific dimensions such as cost codes, locations, and projects to ensure accurate tracking for tax purposes.

For example, if your small business spends heavily on travel expenses, the tool automatically categorizes airfare, lodging, and mileage data, ensuring every deductible dollar is captured.

Integration with Accounting Tools

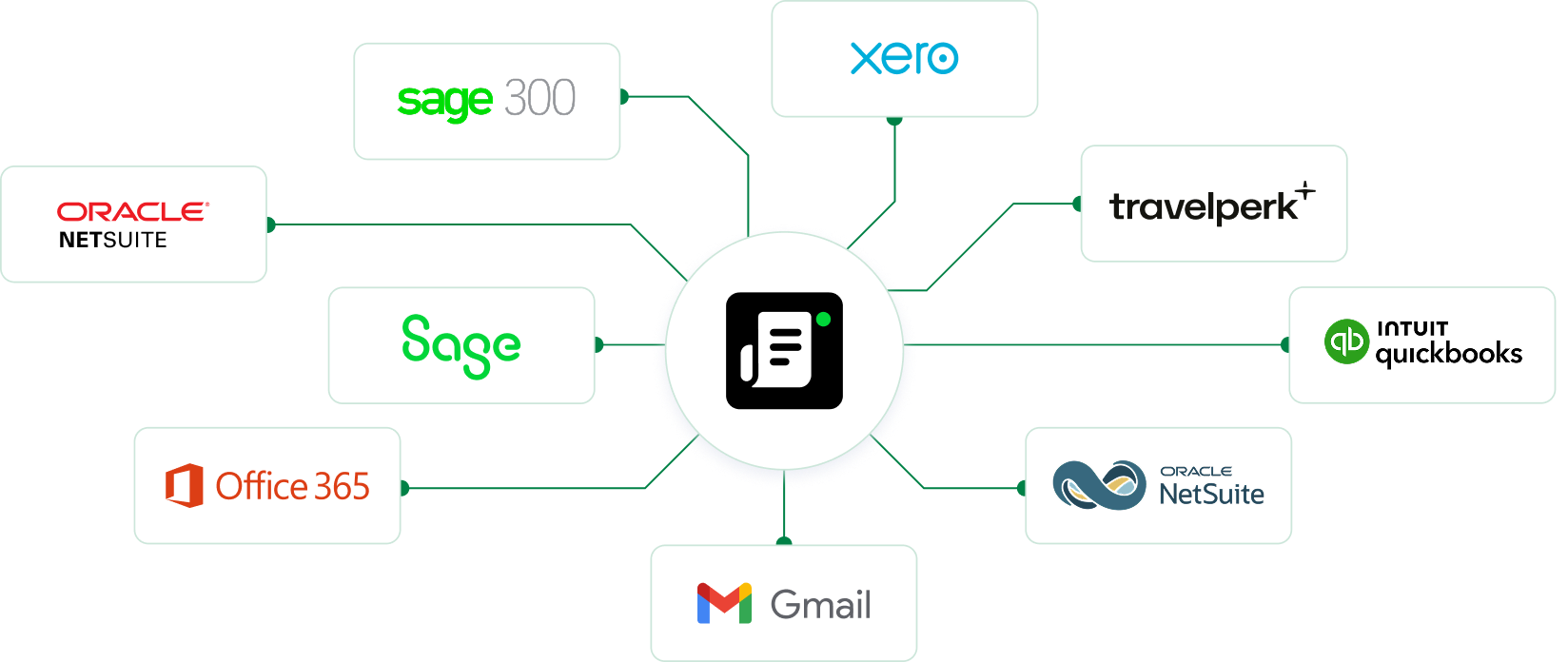

We seamlessly integrates with leading accounting platforms like QuickBooks, Xero, Sage Intacct, and NetSuite, enabling:

- Automatic data imports for employees, projects, and cost codes.

- Real-time exports of expenses such as bills, journal entries, or credit card charges.

- No-code setup with an average implementation time of just 12.6 minutes, ensuring you’re ready to manage expenses without delays.

Why Sage Expense Management is Perfect for Small Businesses

It isn’t just an expense management tool—it’s a tax-time lifesaver for small businesses. Here’s why:

- Streamlined expense tracking: Our intuitive interface ensures that all deductible expenses are logged accurately and categorized appropriately.

- Time savings: By automating receipt collection, credit card reconciliation, and compliance checks, we saves businesses countless hours during tax season.

- Better ROI: With pricing starting at $11.99 per active user per month, it provides unmatched value for its features.

- Instant support: Our customer support team has a 92% CSAT rating and responds within 30 minutes, ensuring help is always available.

In Conclusion

From tracking deductible expenses in real time to ensuring compliance with tax regulations, this platform takes the stress out of managing small business finances.

Small businesses can confidently maximize their deductions and reduce tax burdens by leveraging features like instant receipt collection, automated reconciliation, and real-time spend visibility.

{{manage-business-expenses="/cta-banners"}}

.jpg)